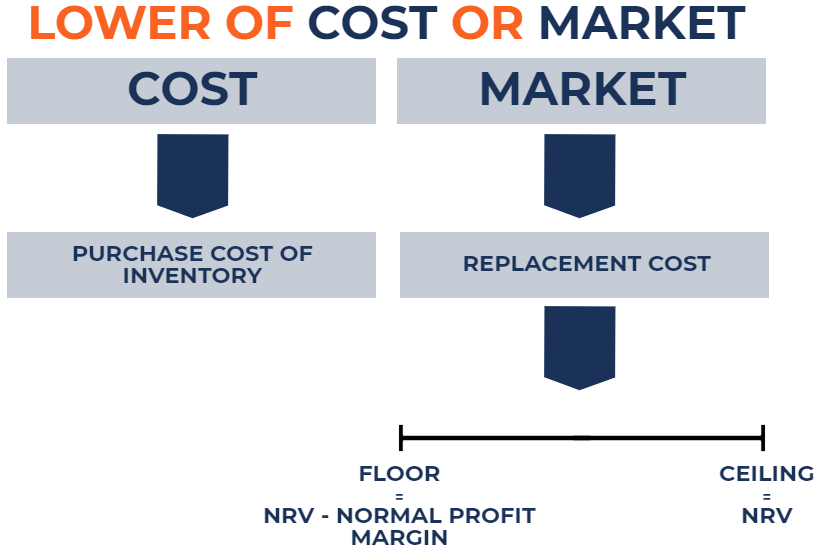

The Floor To Be Used In Applying The Lower Of Cost Or Market Method

Lower Of Cost Or Market Value Rule Lcm Accounting Explained Market Value Marketing Cost

Lower Of Cost Or Market Lcm Definition Inventory Valuation Examples

How To Use Lower Of Cost Or Market Dummies

Lower Of Cost Or Market Rule For Valuing Inventory Youtube

Class 5 Lower Cost Or Market Ppt Download

Lower Of Cost Or Market Lcm Accounting Rule Examples Explained

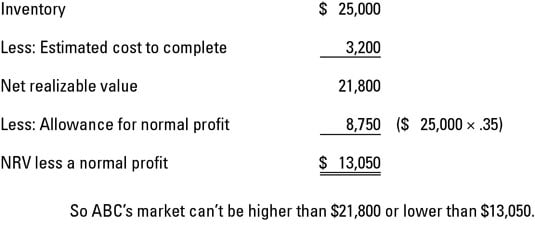

Net realizable value less normal profit margin.

The floor to be used in applying the lower of cost or market method.

Lower Of Cost And Net Realizable Value Lcnrv Open Textbooks For Hong Kong

How To Innovate To Address The 4c Challenge For Rail Innovation Challenges Parker Hannifin

Price Controls Price Floors And Ceilings Illustrated

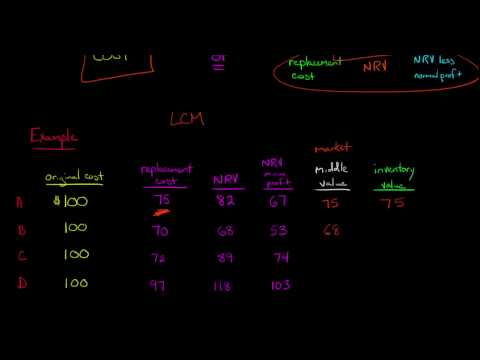

Lower Of Cost Or Market Rule Example Youtube

Borrowers With Cheaper Fha Mortgages Buy Pricier Homes Fha Mortgage The Borrowers Fha Loans

When Launching A New Product The Marketing Mix Also Known As The 4 P S Of Marketing Helps The Firm In Making Strate Marketing Mix P S Of Marketing Marketing

Definition Of Braced Unbraced Columns And Differences Among Them In 2020 Construction Estimating Software Construction Cost Residential Construction

How To Save Energy While Staying Home In 2020 Save Energy Energy Saving Tips Energy

Information Technology It Business Case Credibility And Accuracy Business Case Template Business Case Good Essay

How To Conduct A Swot Analysis Examples Strategies And Templates Swot Analysis Ideas Of Buying A House Fir Marketing Trends Competitive Analysis Marketing

Econ 150 Microeconomics

Beautiful Eichler Inspired Home Draws The Eye With A Dramatic Roof Inspired Homes Inspiration House

19 Little Things That Ll Actually Lower Your Utility Bills Low Flow Shower Head Shower Heads Shower Heads Best

How To Start An Online Business Online Business Start Online Business Business

Dorian Lpg Ltd Lpg Reaches 7 96 After 5 00 Up Move Shorts At Galmed Pharmaceuticals Ltd Ordinary Shares Glmd Lowered By 33 72 Positivity Stock Market Quotes Asset Management

New Study Focusing On Military Virtual Training Market Growth Factors Value Chain Analysis Online Journal News Magazines Alabama News

Pin On Are Structures

Archibus Space Moves Management Facilites Management Services Excitech Limited Facility Management Management Life Cycle Costing

1

Pin On Roofing Charlotte Nc

Mexican Cleft Wallpaper In Indigo Blue Removable Vinyl Wallpaper Peel Stick No Glue No Mess Vinyl Flooring Flooring Floor Stickers

Software Solution Design Process Always Targets Reuse Of Components And Modules To Speed Cloud Computing Technology Web Technology Object Oriented Programming

Unified Modeling Language Diagrams Diagram Pmbok Language

Increase Your Website Traffic And Business Revenue With Attractive Web Designing Development Services Mulsa Web Design Web Design Company Fun Website Design

Source : pinterest.com